Everyone's talking about RWA hitting $31B this week.

Nobody's talking about the RWA project that just went to zero.

➛ The number nobody's posting.

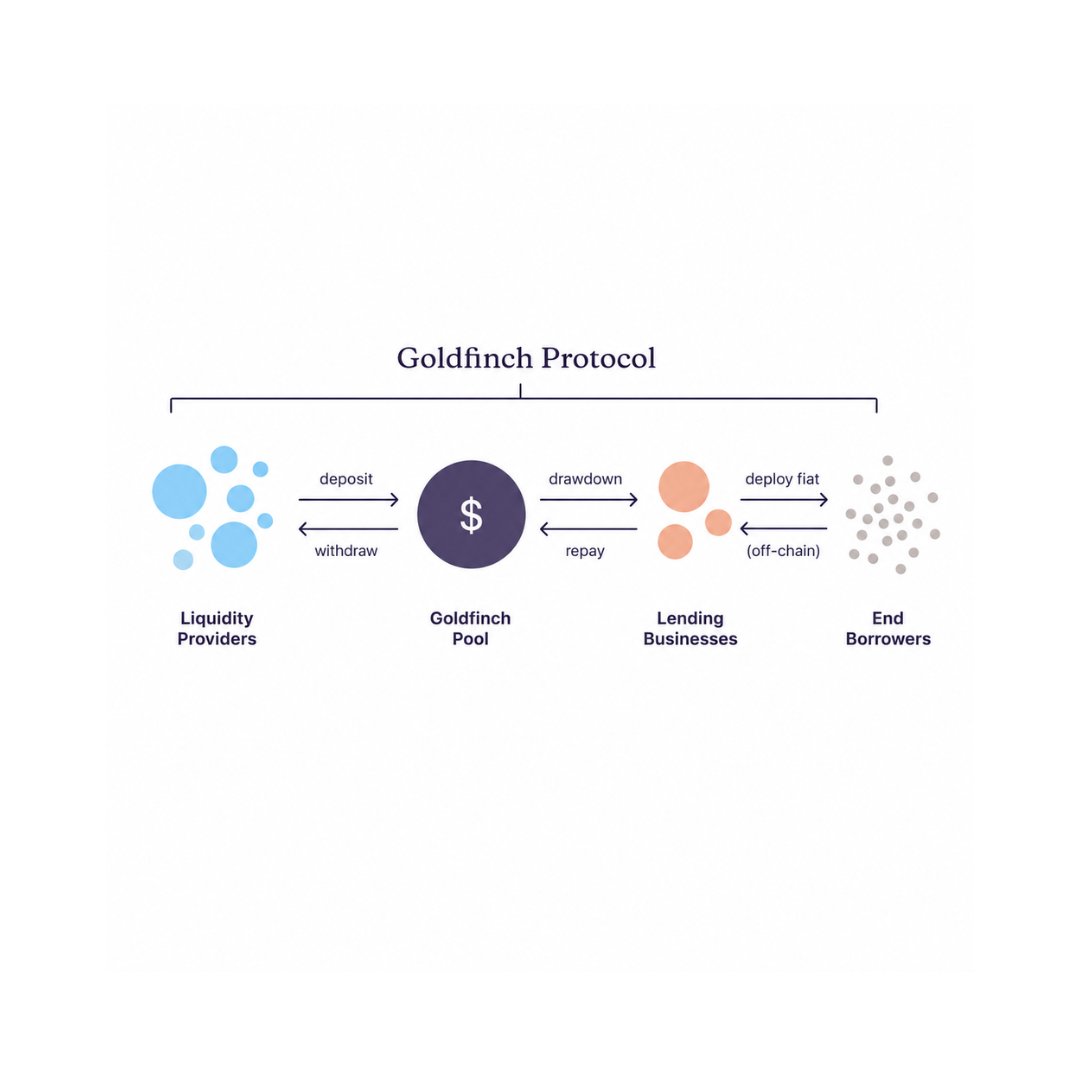

Goldfinch. a16z-backed. The original poster child for "real-world credit, on-chain." The whole pitch was bringing private lending in emerging markets onto the blockchain.

Its token is down 99.8% from ATH. $390M market cap to under $6M.

Of its 8 borrowers, 2 defaulted outright. 6 are in restructuring.

➛ This is happening in the same week as the bull case.

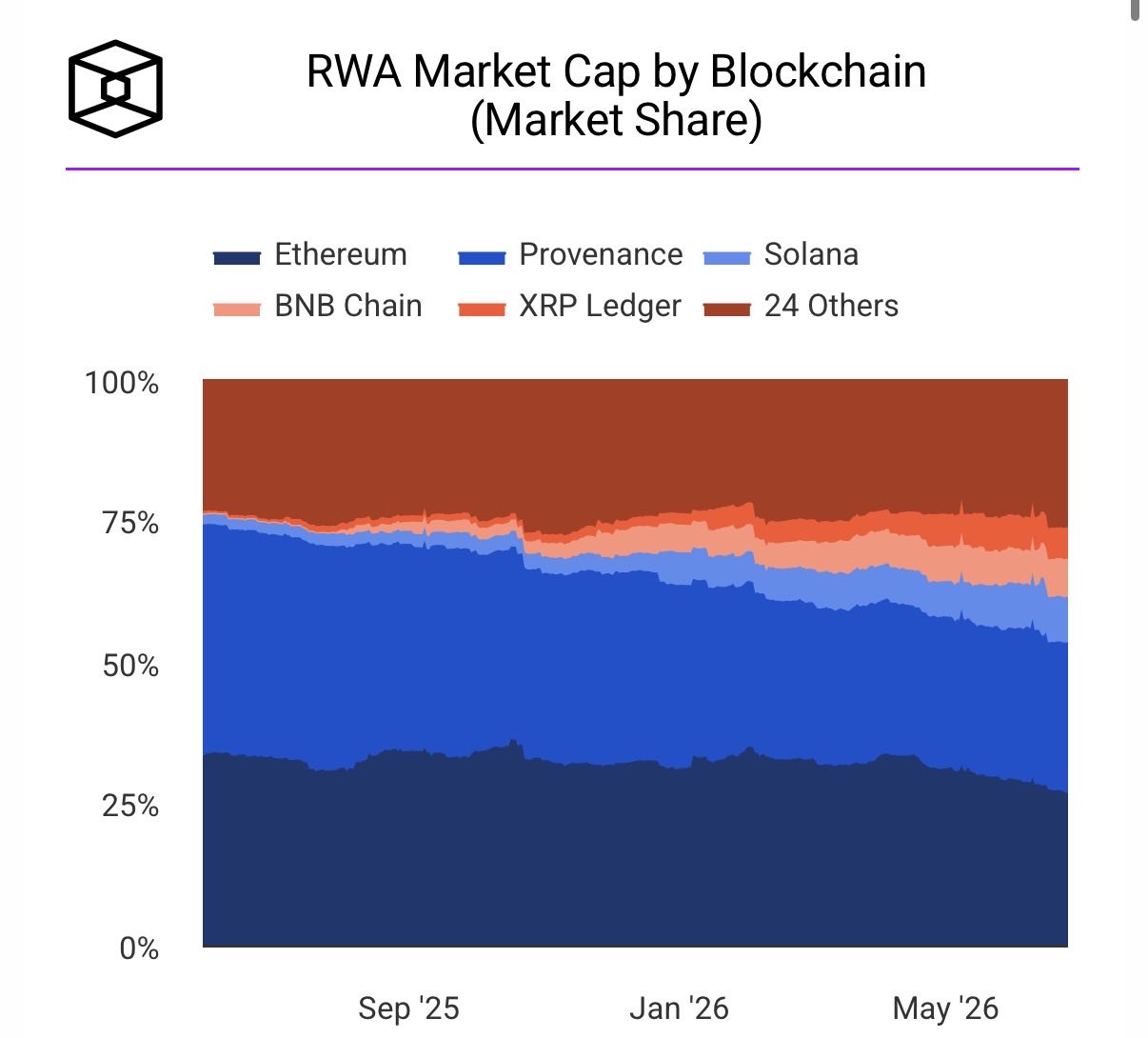

RWA tokenization just crossed $31.4B, up 589% in 18 months. Securitize is going public on the NYSE. Chainlink signed 47 banks for settlement.

Every headline says the same thing: real-world assets are the future.

And they might be. But the future has a failure mode, and Goldfinch is showing you what it looks like.

➛ The part the bull case skips.

You can tokenize a loan. You can put it on-chain, make it transparent, settle it instantly, wrap it in the cleanest smart contract ever audited.

You cannot tokenize whether the borrower pays you back.

That's the thing. RWA's real risk was never the code. It's counterparty risk, the oldest risk in finance, the one blockchains don't remove. Goldfinch didn't get hacked. Its borrowers just didn't pay.

➛ One honest line, because it matters.

Goldfinch is one model, not all of RWA. The $13B in tokenized Treasuries and money-market funds, the part actually driving that $31B is a completely different animal.

Government debt doesn't default like a private credit fund in Africa does. Don't read this as "RWA is dead."

Read it as this: the category is splitting into two. Tokenized Treasuries, where the asset is safe and the wrapper is the innovation. And tokenized credit, where the wrapper is fine and the asset can still go to zero.

The market is about to learn the difference the hard way. Goldfinch is just the first tuition bill.

Which kind of RWA are you actually holding?